UKCS Tiebacks: The Myths Holding Back Development – And the Approaches Redefining What’s Possible

01 Apr 2026

In the first two articles in this series, I explored why subsea tiebacks are now essential in the UKCS, and why delivering them in a mature basin is far more complex than many expect. Yet even when operators understand the urgency and the engineering realities, outdated assumptions still distort decision-making.

These myths shape budgets, influence rig selection, restrict concept thinking and, ultimately, force operators to eliminate options far earlier than they should.

In a basin where the window for development is already tight, these misconceptions cost time, money and strategic opportunity. In this article, I want to challenge them, and highlight how modern subsea thinking, particularly the rise of the circular subsea economy, is transforming what’s realistically achievable today.

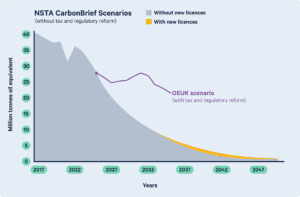

I also think it’s important to note that recent headlines have only reignited debate over the UKCS, as geopolitical instability in the Middle East once again exposes the UK’s reliance on imported oil and gas and our energy security. Much of this discussion has focused on widely circulated charts showing North Sea production declining sharply — often used to argue that issuing new licences would make little difference.

However, I share the view of Offshore Energies UK that projections for the North Sea are shaped as much by fiscal and regulatory assumptions as by geology itself — and that headline decline scenarios do not tell the full story. As shown in the graph below, with proactive tax and regulatory reform, production would still fall, but far more gradually. Set against declining domestic demand, OEUK argues that UK gas could continue to meet a meaningful share of Britain’s needs into the mid‑2030s. With a proactive tax and regulatory reform to support UKCS production, we can have an energy transition that was promised—rather than the current cliff edge for jobs, tax receipts and energy security.

North Sea (UKCS) Production Outlook: NSTA/CarbonBrief Projections With and Without New Licences, with OEUK Output Overlay Under Fiscal and Regulatory Reform

Tax and regulatory reform could:

Improved tax, regulatory environment and new licences for now remain unchanged — we can only hope the Government reconsider the implementation of the energy transition in this regard. For now, one reality remains unchanged: if the UKCS is to deliver what it still can, it’s time to confront the myths that surround subsea tiebacks, and the value they are capable of that are relevant with or without change to the status quo.

Myth #1: “Subsea is too expensive”

Reality: refurbished subsea hardware has changed the cost model.

The circular subsea economy has redefined what subsea solutions look like from a cost and schedule perspective.

Refurbished and redeployed trees and components can now:

For short‑cycle or marginal tieback opportunities, refurbished subsea hardware isn’t a compromise – it’s often the only route that makes the economics work at all. In a basin where remaining resources are smaller and infrastructure is limited, the circular economy is becoming a strategic advantage.

Myth #2: “You can’t drill subsea wells with a jack up”

Reality: jack up drilling for subsea wells is proven, efficient, and widely used.

Across the UK, the Netherlands and multiple APAC basins, jack ups have repeatedly drilled and completed subsea wells in shallow waters. In the UKCS alone, jack up‑to‑subsea operations have become a standard approach because they offer:

I still see operators assuming subsea automatically requires a semi-submersible, when this can be a costly misconception. In today’s market, where clarity, speed and efficiency rule, jack up‑enabled subsea developments can be the difference between a subsea tieback moving ahead or never making it through screening.

Myth #3: “Tiebacks are just simple bolt‑ons”

Reality: UKCS subsea tiebacks are highly constrained and technically bespoke.

No two hosts offer the same opportunity, and no two subsea systems behave the same.

Operators must contend with:

In other words, a UKCS tieback is rarely a “bolt‑on”. It’s a complex brownfield integration exercise requiring careful engineering, robust analysis and a deep understanding of host limitations. In my experience, projects rarely fail because the reservoir is wrong – they fail because the well life cycle well access (development drilling, intervention and abandonment) and the engineering between seabed and host platform was underestimated.

The circular subsea economy: the new model reshaping UKCS tiebacks

The circular subsea economy is already changing how operators think about cost, schedule and sustainability. Its advantages include:

It’s important to note that a refurbished tree rarely comes back perfect or will match every operator’s internal specifications – and it doesn’t need to if safety and regulatory factors are met. Operators must learn to compromise if they want to unlock marginal fields and re-use subsea hardware across multiple wells. An “80% good” configuration keeps a project alive, while waiting for 100% optimised full operator internal specification compliant system can stall it completely. From what I see across the basin, pragmatic engineering is now a competitive advantage in the UKCS.

Unlocking the advantages of refurbished hardware also depends on having the right engineering and interfaces in place. Intelligent engineering and tooling ensure that reused equipment integrates safely with ageing hosts, particularly where structural capacity or riser geometry is already constrained.

Final thoughts

The UKCS doesn’t lack tieback potential – it lacks clear visibility past the myths that limit innovation. By breaking away from outdated assumptions, embracing circular subsea principles, and designing subsea tiebacks around the real, late‑life infrastructure of the basin, operators can bring new life to assets that still have value left to give.

Unless proactive taxation and regulatory reform are implemented, which will support UKCS production more broadly and the energy transition promised, subsea tiebacks are one of the only options available to extend a field’s economic life. The next generation of UKCS subsea tiebacks won’t be defined by scale, but by how decisively operators move beyond ideology and outdated assumptions to integrate existing infrastructure and unlock the value that remains.

If you’re exploring a tieback opportunity or simply want clarity on what’s feasible within your existing host constraints, I’m always happy to discuss the practical realities and help shape the path forward.

–

Sky News (2026). North Sea oil: Is it time to reconsider drilling? [Online]. Available at: https://news.sky.com/story/north-sea-oil-is-it-time-to-reconsider-drilling-13520893 [Accessed Mar. 2026].