Rethinking Field Development in a Changing UKCS: Clusters, Slot Recovery & Short-Cycle Projects

20 Apr 2026

In the earlier articles in this series, I’ve focused on why subsea tiebacks are now the only “development” well drilling option in the UKCS if an operator wants to extend production, and the engineering realities that determine whether they succeed or fail. But sustaining development in this basin requires thinking beyond individual tiebacks.

With constraints tightening, the UKCS does still present several viable pathways to extend host platforms and infrastructure life, preserve export routes, and keep subsea tiebacks commercially and technically viable – provided operators are prepared to think beyond conventional development models, even within the current tax and regulatory environment.

Clustered subsea developments: when multi well templates deliver what single wells can’t

The industry often thinks of tiebacks in terms of one well, one flowline, one umbilical. In my experience, clustered subsea developments, where a group of wells is drilled from a single template, frequently offer advantages that single well tiebacks cannot match.

Why clusters matter in a late life basin:

In a UKCS where hosts are shutting down faster than new projects progress, a reality I outlined at the start of this series, clusters create the scale that keeps subsea tiebacks alive, not just technically, but commercially. There are plenty of examples of shallow-water jack-up drilled subsea well clusters in the UKCS and Norway, such as the Catcher Field, with 4 subsea wells per drill centre template and Ekofisk, with 8 subsea wells per drill centre template.

Of course, not every project will want all wells on one drill centre, as an advantage that subsea wells have is that they can be positioned over a hydrocarbon deposit to simplify drilling, but this needs to be evaluated against other project costs to determine the best solution for a specific project.

Slot recovery and slot addition: extending platform life without new steel

Slot recovery – reinstating, reusing, or re-entering existing well slots on fixed platforms – is one of the UKCS’s most overlooked advantages.

Aging platforms often retain significant potential even when new structural additions are impossible or uneconomic.

Slot recovery enables:

In a basin where marginal production economics exist, slot recovery or slot addition is an agile, cost-effective way to extend platform life and a potential addition or alternative to a subsea tieback.

Small pockets, big impact: short‑cycle shallow‑water projects

Not every development needs to be large. In fact, many of the UKCS’s remaining hydrocarbon opportunities are small, short-cycle pockets that can deliver meaningful economic impact if developed intelligently.

These shallow water subsea wells typically use:

These projects:

In a declining basin, these small wins compound into significant strategic impact. Add to this the circular economy philosophy and the subsea hardware refurbishment industry that is growing rapidly, these subsea trees and other hardware can be serviced and re-deployed onto the next project greatly increasing project economics and standardising project scopes.

A new playbook for UKCS field development

Subsea tiebacks remain central to the UKCS future – but they cannot thrive in isolation. From what I see across the basin, it requires a development playbook suited to its late life realities:

The modern UKCS development toolkit:

These approaches collectively achieve what no single method can deliver in the current UKCS tax and regulatory environment:

This is how, via an intelligent combination of small, modular, and strategic development choices, UKCS extends its productive life as larger new projects are effectively off the table due to current punitive taxation, no new licences and regulatory environment.

Final thoughts

The UKCS is entering a more complex, constrained, and time-sensitive phase of its life—yet it remains one that still presents opportunity for operators willing to think differently.

In my experience, clustered subsea developments, slot recovery and addition, and short-cycle shallow-water projects are becoming the backbone of a modern, flexible development strategy in the UKCS. They support tieback viability, extend host life, and create optionality in a basin that increasingly demands agility over scale. Unlocking that value depends on moving beyond outdated assumptions and designing operations around the basin’s evolving realities.

With tieback strategies now covered, it’s also worth revisiting how more operators are beginning to question the role of exploration in the North Sea—particularly in light of recent geopolitical shifts.

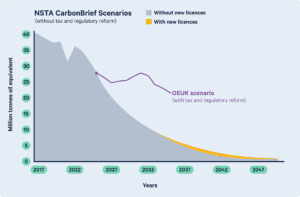

As discussed earlier in this series, widely cited production outlooks from the NSTA and Carbon Brief are often used to frame the basin as offering diminishing returns from new exploration.

However, I share the view of Offshore Energies UK that projections for the North Sea are shaped as much by taxation and regulatory policies as by geology itself — and that meaningful value remains to be unlocked. Recent OEUK analysis suggests that, with the right policy framework, the UK could significantly increase domestic oil and gas production over the coming decades, as shown in the graph below, strengthening energy security at a time of heightened geopolitical uncertainty and reducing reliance on imported LNG, which typically carries greater exposure to global market volatility.

North Sea (UKCS) Production Outlook: NSTA/CarbonBrief Projections With and Without New Licences, with OEUK Output Overlay Under Fiscal and Regulatory Reform

In conclusion, I think the current challenge facing the North Sea is ultimately less about resource scarcity and more about strategic choice, whether that’s via tiebacks, or within new exploration. If you’d like to explore how the approaches discussed throughout this series could reinvigorate your assets, or how they fit into a wider tieback strategy, I’d be very happy to discuss the practical considerations and help shape the most effective path forward.

–

Sky News (2026). North Sea oil: Is it time to reconsider drilling? [Online]. Available at: https://news.sky.com/story/north-sea-oil-is-it-time-to-reconsider-drilling-13520893 [Accessed Mar. 2026].